IMARC Group has recently released a new research study titled “United States Chronic Disease Management Market Size, Share, Trends and Forecast by type, disease type, deployment type, and end user., and Region, 2025-2033” which offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends, and competitive landscape to understand the current and future market scenarios.

Market Overview

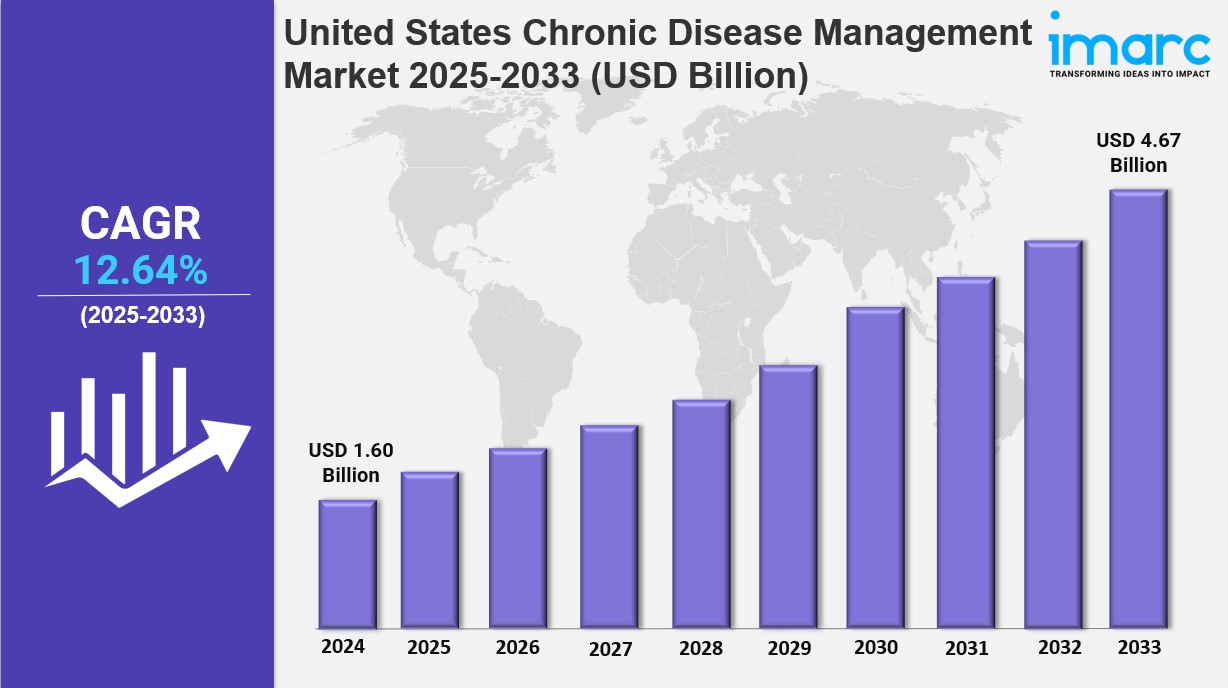

The United States chronic disease management market size was valued at USD 1.60 Billion in 2024 and is forecasted to reach USD 4.67 Billion by 2033, exhibiting a CAGR of 12.64% during the period 2025-2033. Growth is driven by the rising adoption of remote patient monitoring and personalized treatment plans enhancing care outcomes and efficiency. This market shift highlights proactive, data-driven care models, improving patient engagement and reducing hospital visits.

Study Assumption Years

- Base Year: 2024

- Historical Year/Period: 2019-2024

- Forecast Year/Period: 2025-2033

United States Chronic Disease Management Market Key Takeaways

- Current Market Size: USD 1.60 Billion in 2024

- CAGR: 12.64% from 2025-2033

- Forecast Period: 2025-2033

- The rising demand for remote patient monitoring (RPM) enables real-time tracking and early intervention.

- Healthcare providers are prioritizing personalized treatment plans tailored to individual needs.

- Digital health technologies like wearables and AI tools are revolutionizing chronic care delivery.

- Cardiovascular diseases represent the largest disease type segment with a 29.1% share.

- On-premises deployment dominates with a 49.8% share due to data security and customization.

- Healthcare providers hold 78.2% of the market share as primary end users.

Sample Request Link: https://www.imarcgroup.com/united-states-chronic-disease-management-market/requestsample

Market Growth Factors

The growing prevalence of chronic conditions and also aging populations substantially drive at the market. One chronic condition was reported in 2023 by 76.4% of U.S. adults. The percentage increased up to 93% among older adults. This trend elevates the demand for such continuous and long-term care systems that stress integrated and proactive approaches including multidisciplinary care teams, lifestyle interventions, and personalized treatment plans. Healthcare systems are investing throughout infrastructure. Workforce investments are also required given these evolving chronic care needs.

Preventive health focus and value-based care shift aid the market. Proactive management of chronic diseases occurs if providers improve health outcomes rather than service volume. Care strategies for preventive methods diagnose conditions early, and such strategies guide lifestyles in order to limit complications, plus they reduce interventions that are costly for emergencies. Due to policy reforms along with reimbursement reforms, there is support for care coordination programs and also patient education platforms plus multidisciplinary services, so they can enable chronic disease management solutions that happen to be sustainable and scalable.

Demand is additionally fueled by AI-driven technologies along with digital health advancements. Telehealth platforms along with wearable devices and even mobile applications enable real-time monitoring as well as remote consultations. In 2024, 66% of U.S. physicians use AI tools, almost doubling since the previous year, and these tools improve clinical decision-making and personalized care. Digital tool integration with electronic health records improves care coordination, efficiency, also patient empowerment. Because these tools are integrated, it also transforms chronic disease management into a connected, patient-centered system.

United States Chronic Disease Management Market Segmentation

Analysis by Type:

- Solutions

- Services

*Solutions* include software platforms, digital tools, and remote monitoring technologies enhancing diagnosis, monitoring, and tailored care coordination. *Services* cover clinical support, care coordination, patient education, and consulting by healthcare professionals or third parties, ensuring continuous treatment compliance and customized care delivery.

Analysis by Disease Type:

- Cardiovascular Diseases

- Diabetes

- Cancer

- Asthma

- Chronic Obstructive Pulmonary Disorders

- Others

*Cardiovascular diseases* hold the largest share of 29.1%, driven by prevalence and need for continuous monitoring, lifestyle management, and medication adherence. These conditions require comprehensive care coordination and frequent patient engagement, with government initiatives promoting targeted chronic care.

Analysis by Deployment Type:

- On-premises

- Cloud-based

- Web-based

*On-premises* dominate the market with a 49.8% share due to demand for greater control, security, and customization of patient data. This setup supports compliance with data privacy laws such as HIPAA, reliable performance in low connectivity sites, and integration with hospital systems.

Analysis by End User:

- Healthcare Providers

- Healthcare Payers

- Others

*Healthcare Providers* account for 78.2% of the market due to their central role in diagnosis, treatment, and ongoing management of chronic conditions. Their infrastructure enables integrated care models and remote monitoring effectively.

Breakup by Region:

- Northeast

- Midwest

- South

- West

Regional Insights

The Northeast is dominant in the market, benefiting from a high concentration of advanced healthcare facilities, academic medical centers, and strong policy support. This fosters demand for integrated care, digital health solutions, and personalized treatment services supported by high insurance coverage and an aging population.

Ask an Analyst: https://www.imarcgroup.com/request?type=report&id=20387&flag=C

Recent Developments & News

- May 2025: FDA and NIH launched the Nutrition Regulatory Science Program targeting chronic disorders linked to food, aiming for evidence-based policies to improve health outcomes.

- May 2025: Sumitomo Corporation acquired full ownership of ActivStyle, expanding its U.S. healthcare portfolio focusing on home medical supplies for chronic conditions.

- April 2025: Longevity Health Holdings merged with 20/20 BioLabs to enhance chronic disease risk management and early cancer detection services, valuing the combined entity at $99 million.

- February 2025: Owens & Minor launched ByramConnect, a digital health platform powered by the Welldoc App for chronic condition management.

- February 2025: Biocon Biologics introduced YESINTEK, a biosimilar to Stelara in the U.S. for conditions like Crohn’s disease and psoriasis.

- February 2025: ScienceSoft delivered the MVP of VitalOp Wellness, a chronic disease management platform featuring health tracking and personalized content.

Key Players

- Sumitomo Corporation

- ActivStyle

- Longevity Health Holdings

- 20/20 BioLabs

- Owens & Minor

- Biocon Biologics

- ScienceSoft

Customization Note

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

Tel No: (D) +91 120 433 0800,

United States: +1-201971-6302